Clay's $5B Tender: What It Means for Mid-Market Outbound Stacks

A $100M Series C in August at $3.1B, then a second tender at $5B five months later. What the 3.3x step-up signals about 2026 pricing for mid-market Clay customers.

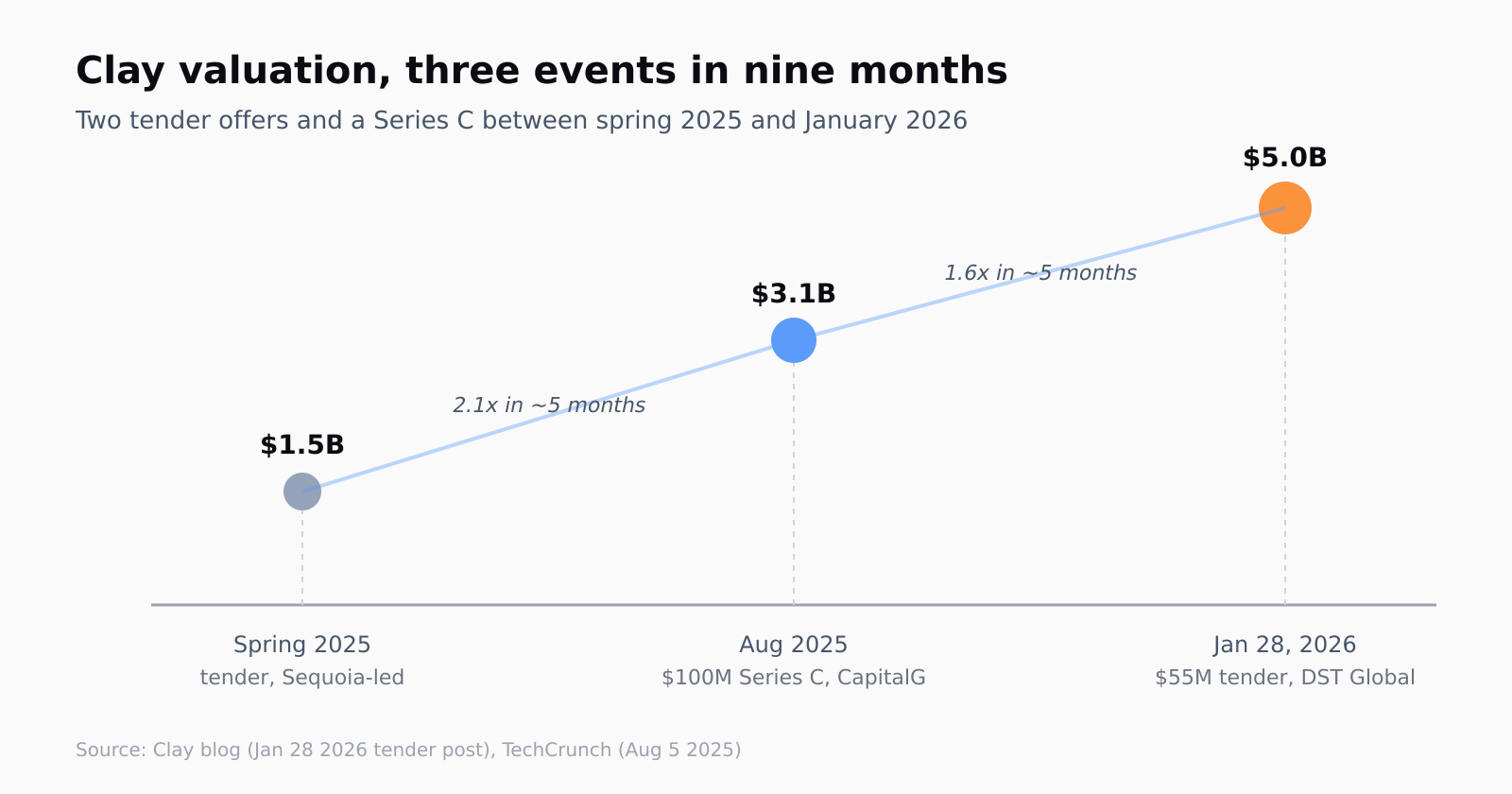

Clay closed its $100M Series C in August 2025 at a $3.1B post-money, led by CapitalG. Five months later, on January 28, 2026, the company ran its second employee tender offer in nine months - $55M of secondary at a $5B valuation, this time led by DST Global. That's a 3.3x mark-up on the round and a 3.5x mark-up on the prior tender (a Sequoia-led $1.5B clearing price last spring), and it's the more interesting of the two numbers if you're a mid-market team writing the 2026 outbound budget right now.

The Series C was a normal-shaped round for a category leader: CapitalG lead, existing investors (Sequoia, Meritech, First Round, BoxGroup, Boldstart) ratable, Sapphire Ventures new, $204M total raised across the company's life. The tender is the unusual move. Repeat secondary tenders nine months apart at a 3x mark-up are, as Clay itself put it, "extremely rare" - and the framing the company chose says a lot about what the next 12 months look like for buyers.

From the tender announcement:

This tender is designed to give our team the flexibility to use the value they create every day. Whether it's buying a home, taking care of family, funding a passion project, or simply getting more breathing room, we want people to have options when life calls for them. [...] We believe that companies hitting their milestones should offer equity as part of people's journey, not just at the end. And we want all our employees to benefit meaningfully from the value they create.

Two things to read out of that. First, Clay is publicly committing to staying private for a while longer - you don't run a second tender at a 3x step-up if an S-1 is on the desk. Second, the named individual investors on the new round (Stripe's Claire Hughes Johnson, Figma CMO Sheila Vashee, Superhuman CEO Shishir Mehrotra, product lead Lenny Rachitsky) are the kind of cap-table that signals "we plan to be a public software company eventually," not "we plan to sell." Both of those are good news for a buyer whose 2026 stack assumes Clay will still be around in 2028.

The growth metrics Clay cited alongside the tender are the part you should actually pin to the wall, because they predict your invoice. Revenue more than 3.5x'd last year and crossed $100M ARR in December 2025. Enterprise net revenue retention is above 200% (which means existing enterprise accounts are roughly doubling their Clay spend year-over-year - _not_ from seat growth alone; that's credit consumption inside accounts). The company says it's cash-flow positive for parts of the year and earns more in interest than it burns. Customer count is 14,000. Zero enterprise customer churn (!). Those are extraordinary numbers and there is no honest skeptical read of them - Clay is, by every public metric, winning the GTM-tooling category right now.

So what does a 3x step-up on a category-winning private company mean for a mid-market team that's already on Clay, or weighing it against the rest of the outbound stack comparison we ran earlier this year?

The mechanical thing first. A $5B private valuation on $100M ARR is a 50x revenue multiple - well above the public-comp band for SaaS even on the optimistic end, and broadly in line with where investors price companies that are expected to roughly double again in the next 12-18 months. To grow into that multiple, Clay has to keep its NRR engine running, which means continuing to push credit-cost-per-row up inside existing accounts. The 200%+ enterprise NRR didn't appear by accident. It is the product of (a) more workflow templates getting wired into more teams inside the customer, (b) higher per-row credit costs as AI features get pushed deeper into the platform, and (c) annual contract resets that bake last year's overages into the new floor. None of those three levers is going away in 2026.

For a mid-market buyer who's already on a self-serve or Starter plan, the practical implication is that the gap between the published price and what an enterprise account actually pays Clay is going to widen, not narrow, through 2026. I'd budget for a Q2 or Q3 plan-tier restructure - I'm not predicting specific numbers because Clay hasn't pre-announced any, but new investors of the DST type don't sit on a cap table for nine months without seeing a pricing motion, and Clay's existing pricing page already runs five tiers from Starter to Enterprise with credit-based metering layered on top. A simpler way to say this: if your renewal is coming up in the back half of 2026, lock the multi-year now rather than after the next pricing-page update.

This is the seam Leadex was built to sit at - the gap between "Clay can do everything if you can afford it and have a RevOps engineer to build the columns" and "we need a list of 500 prospects by lunch." Leadex is a chat-native B2B lead research agent: you describe the ICP in plain English, the agent drafts a research plan, you approve it, and a deduped CSV lands in your CRM. No spreadsheet maintenance, no per-row credit metering, no five-figure annual minimum to unlock the features you actually use. We wrote about the practical tradeoff in Clay alternatives for teams without a dedicated RevOps engineer last quarter; the tender announcement makes that piece more relevant, not less.

Two caveats on the bear case. The "tender offers signal exit fatigue" narrative does not fit Clay's specifics. The company's framing - equity-as-journey, not equity-at-end - reads as a deliberate retention play in a market where senior IC engineers have been the scarcest resource at any AI-adjacent company for two years running. And the fact that the round was upsized to bring in a named growth investor like DST (which has historically led pre-IPO crossover rounds at exactly this stage) is more consistent with "stretching the runway to a 2027-2028 IPO window" than with "preparing for an early sale." If you're a Clay customer who reads tenders as bearish: this one isn't.

The thing I'd keep an eye on instead is the GTM Engineer positioning Clay has been pushing since the Series C. The narrative - one GTM engineer can amplify 100 sellers, $160k median salary, 400+ open roles as of mid-2025 - is doing the same work for Clay that "DevOps engineer" did for HashiCorp a decade ago: it justifies the per-seat and per-credit cost by claiming a new headcount line item. That's coherent for a 1,000-seat customer with an internal GTM platform team. It's less coherent for a 12-person mid-market shop that doesn't have anyone whose full job is writing Clay templates. The 2026 tier-pricing motion, when it lands, will almost certainly target the gap between those two customer profiles - pricing the heavy enterprise build-outs as a premium tier and pushing the small-team users toward a simpler self-serve floor. Worth knowing now, not at renewal.

The pre-tender Clay customers I've talked to mostly fall into two camps: those who have already hired or appointed a GTM engineer and are going to be fine through any price restructure, and those who are running Clay as a faster Apollo and will feel the floor moving up. If you're in camp two, the AI lead generation tools we ranked earlier this year covers the practical alternatives at the chat-first end of the market; the half I'd flag for re-reading is the section on tools that don't charge per-row.

One last thing worth noting from the Clay disclosure: 150 agencies and 90 international clubs. The community moat is the part that's hardest to compete with on price alone - a tooling decision that has 90 in-person meetups defending it is not the kind of thing a procurement-led RFP unseats. The 2026 pricing motion, when it comes, is going to be threading a needle between "monetize the heavy users" and "don't crack the community flywheel." Watch the Q2 release notes more than the press releases for the actual signal.