How to Find Companies That Just Got Acquired (M&A Signal Playbook)

Post-acquisition is a documented 90-day buying window - integration deadlines, redundant line items, and procurement reviews hit at once. The hard part isn't detecting deals (8-K Item 2.01, Crunchbase, PR Newswire all work) - it's filtering the firehose by ICP before chasing anything.

On January 29, 2026, G2 announced it was acquiring Capterra, Software Advice, and GetApp from Gartner, with the deal expected to close in Q1 2026. Three months later, every vendor whose product touches a Capterra listing - review-collection tools, PPC-on-software-categories agencies, lead-routing middleware, taxonomy-mapping services - is sitting on a buying window that will not be open for long.

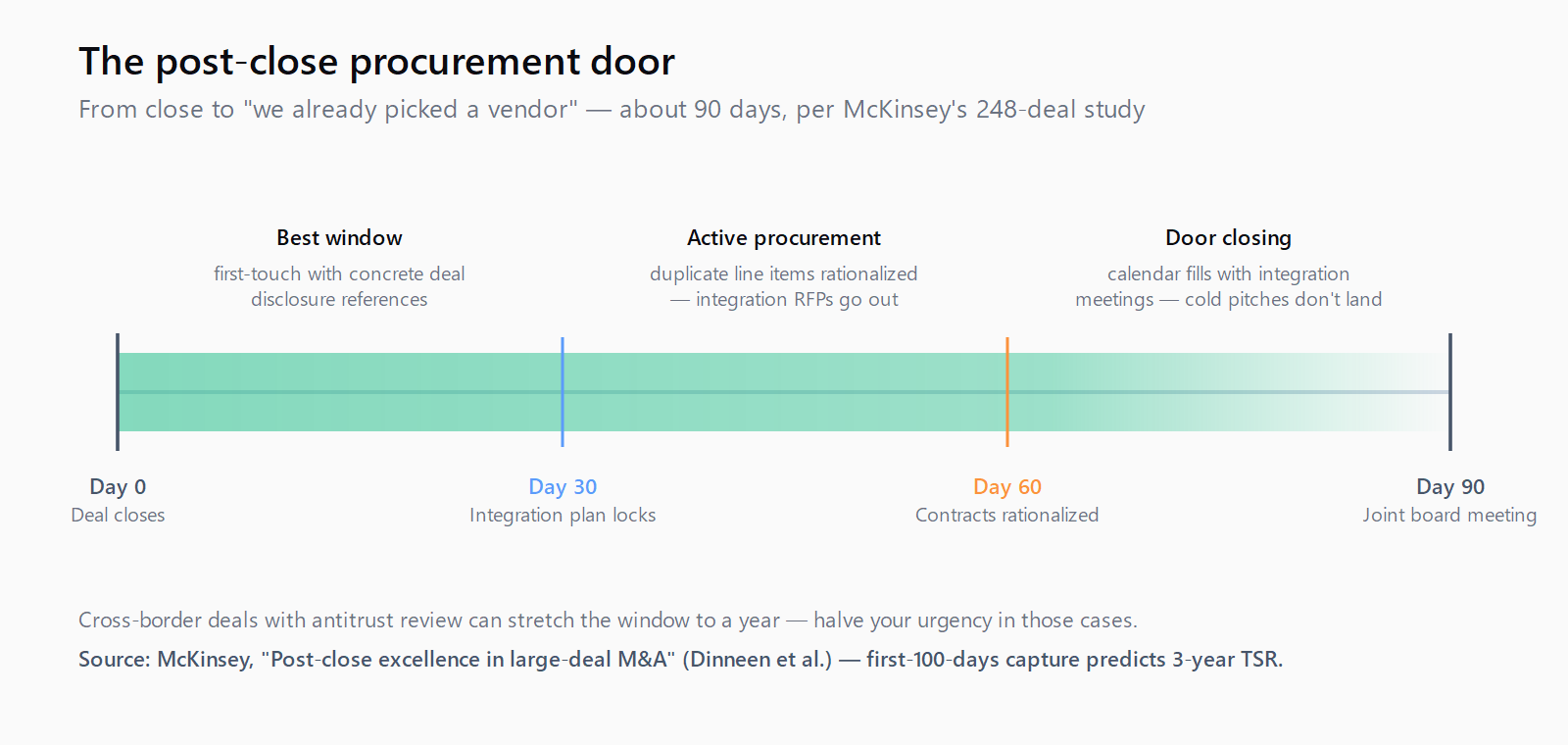

That window has a name in the consulting literature. McKinsey's 248-deal study, "Post-close excellence in large-deal M&A" by Brian Dinneen and co-authors, found that companies which captured most of their planned cost and revenue gains inside the first 100 days were the ones whose total return to shareholders stayed above the market three years later. The acquired side spends those 100 days picking which contracts to keep, which to consolidate, and which integrations need to exist by quarter-end. That's the procurement equivalent of an open door, and it closes around day ninety.

The buyer's-side view of that window is brutal. Maria Akhter, who runs revenue best-practices content at Outreach, wrote a piece in February on what RevTech vendor mergers actually feel like to the customer. The two sentences worth pinning above your monitor:

When two RevTech tools need to become one, your sales team is at the mercy of vendor timelines. [...] Platform mergers usually kill innovation velocity.

- Maria Akhter, Editor, Revenue Best Practices, Outreach

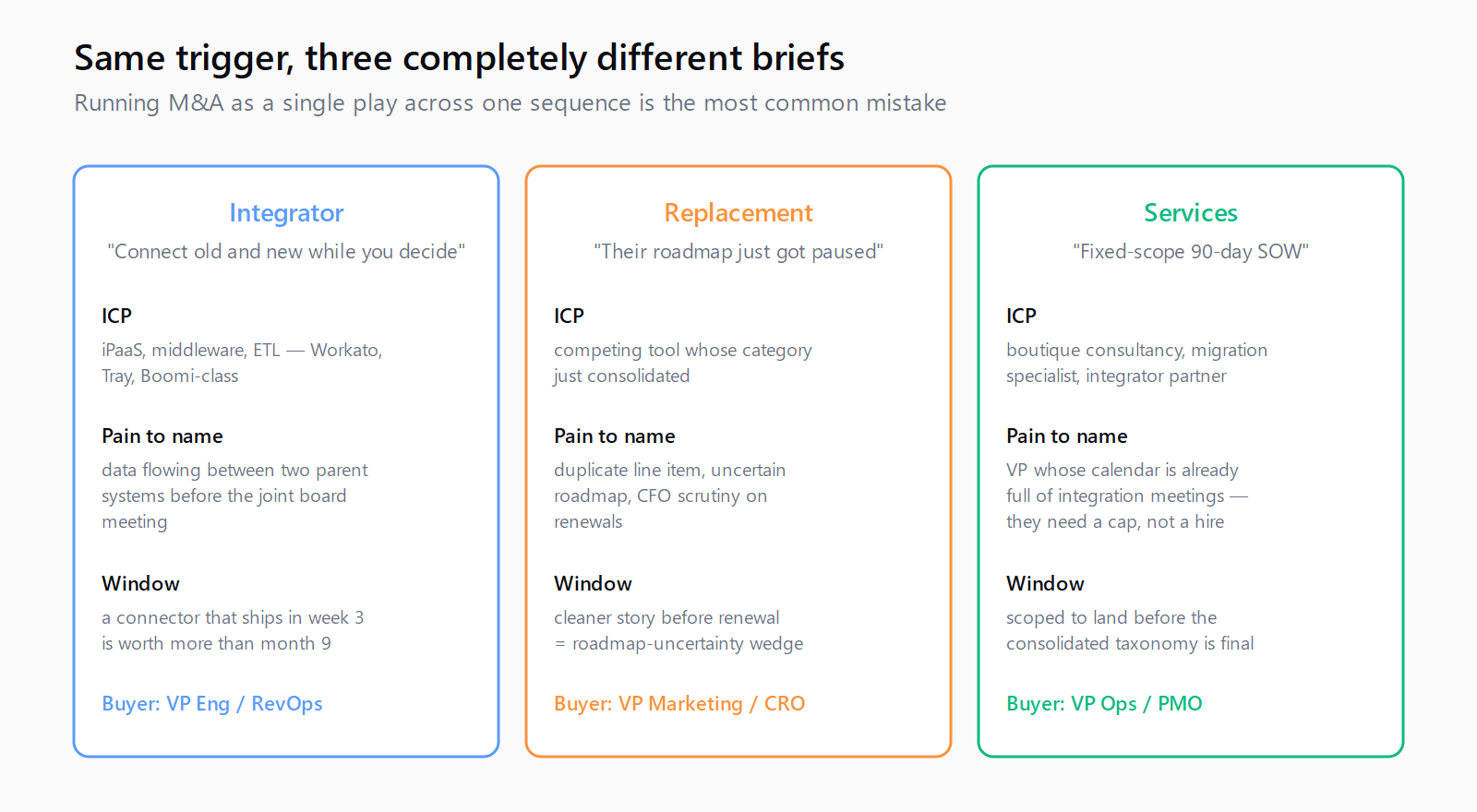

Translate that to a seller's checklist. A company that just got acquired is staring at three problems at once: their incumbent tool's roadmap is now uncertain, their internal stack has duplicate line items the new CFO will rationalize, and someone needs to bridge the data between the two parent systems before the first joint board meeting. Each of those is a different sale. The integrator pitches "we connect old and new while you decide." The replacement vendor pitches "the redundant line item is the one whose roadmap just got paused." The services firm pitches "fixed-scope 90-day SOW to land you on the other side." Same trigger event, three completely different briefs.

Take the G2 deal as the worked example. An iPaaS vendor (Workato, Tray, Boomi-class) goes in as the integrator: the listing data on Capterra needs to merge cleanly with G2's review schema, somebody has to keep both pipelines flowing for six months while the merge happens, and a connector that ships in week three is worth more than one that ships in month nine. A category-leadership PPC tool goes in as the replacement: any vendor currently spending six figures a quarter on Capterra category pages is going to ask whether their bid stack still makes sense under one combined taxonomy, and if a competitor pitches a cleaner story before the renewal, the incumbent's roadmap-uncertainty is the wedge. A boutique consultancy goes in as services: a fixed-scope review-data migration audit at $50k flat, scoped to land before the consolidated taxonomy is finalised, written for a VP-Marketing whose calendar is already full of integration meetings. None of those three pitches works for the other two ICPs, which is why running M&A as a single play across a single sequence is the most common mistake I see.

Detection is the easy part. The SEC's EDGAR full-text search indexes every 8-K filed under Item 2.01 ("Completion of Acquisition or Disposition of Assets") inside the four-business-day window the rules require. The same query also catches Item 1.01 ("Entry into a Material Definitive Agreement") if you want to see deals at announcement, not close - I'd recommend monitoring both, because the announcement-to-close gap is itself useful intel for sequencing. Crunchbase covers the private-side deals EDGAR misses, with a "recent acquisitions" feed that's adequate for free-tier monitoring and an API for anything beyond that. PR Newswire and Business Wire round out the mid-market deals that don't trip either filter, and Mergr or PitchBook are worth the subscription if your ICP skews lower-mid-market where SEC coverage thins out. Wire all three (or all five) into a Monday-morning digest and you have a complete picture of the prior week's M&A activity in the geographies and sizes you care about.

Relevance is the actual work. This is where most M&A-as-trigger plays fall apart - the 8-K firehose is enormous, the average deal in it has nothing to do with your ICP, and a rep who chases everything ends up with a research budget burned on companies that were never going to buy. The fix is to run the ICP filter first and the M&A filter second, not the other way around. Start from the named-account list you already trust, then check that list against last week's filings; the cross-section is short, specific, and worth the personalised first-touch email. This is the same shape as stacking signals generally - any single trigger is too noisy to act on alone, and an acquisition trigger that hits an off-ICP company is just noise wearing a suit.

This is the sort of multi-source brief - parse the 8-K feed, cross-reference Crunchbase, filter by the named-account list, enrich with headcount and tech-stack, route through the right persona play - that we end up running constantly inside Leadex. The shape on our side is familiar: describe the brief in chat, the agent shows you a plan preview with the exact sources and tools it will hit before any spend, you approve, and a deduped CSV lands in HubSpot tagged by which of the three plays (integrator, replacement, services) the row qualifies for. The brief travels with the conversation, so a follow-up like "now exclude the ones we've already pitched" works without re-stating context.

One more practical note on first-touch sequencing. The first email after an acquisition closes should not be the standard outbound template with "congrats on the news" pasted on top. The buyer is, by week two, getting a few dozen of those, and they read identically. The version that gets a reply is shaped to which of the three plays you're running and references something specific from the deal disclosure - the named integration milestone in the 8-K, the line in the press release about consolidated reporting, the analyst commentary on which side's product is the survivor. That research is the work; the email itself is a paragraph. The first seller who is concretely useful inside the first thirty days, per the same trigger-event literature that the UserGems guide compiles, wins disproportionately - not because anyone said the first email had magic powers, but because by week six the buyer's calendar is full of integration meetings and a cold pitch from a vendor they've never heard of doesn't make the cut.

The fair counter-take, for anyone tempted to bolt an M&A monitor onto an outbound process tomorrow: most M&A is irrelevant to most vendors. A vertical SaaS roll-up in healthcare staffing is not your signal if you sell devtools. The signal becomes high-value only when it intersects an ICP fit you've already validated - same logic as the broader buying-signals taxonomy, where a trigger without context is at best a curiosity. M&A is also a slower trigger than, say, tech-stack displacement picked up from a Wappalyzer diff; the buyer who already swapped their CRM is committed, the buyer whose parent just got acquired is still negotiating who's allowed to sign the contract. Plan your first-touch language accordingly. (And if the deal is enormous and cross-border, halve your urgency - antitrust review can stretch the window to a year, and the procurement door doesn't really open until the regulators are done.)

Pull last week's 8-K filings now, intersect them with your top-100 list, and read whichever rows survive. The list is shorter than you think, and the three calls that come out of it write themselves.